AEON, the Japanese retail giant with annual revenue approaching RMB 500 billion and a global ranking within the top 20, rarely seems to feature in public discourse.

Over the past three decades, Japan’s retail landscape has undergone continual transformation, with discount stores, drugstores, convenience stores, and other formats constantly evolving. Traditional retailers and supermarkets have either downsized or been forced to close.

Yet AEON, which began as a traditional general merchandise retailer, has not contracted. Instead, it has sustained continuous growth and reinvention, emerging as the undisputed leader of Japan’s retail industry.

In the retail world, attention tends to gravitate toward 7-Eleven, Costco, or Walmart. Armed with standardized models that have conquered markets worldwide, they might be described as retail’s “one-punch heroes.”

AEON is different. This understated giant has pursued an extraordinarily complex path of constant transformation, deeply rooted in local markets. Its story is, above all, a story of adaptation.

The greatest gap in public understanding of AEON lies hidden in its financial statements.

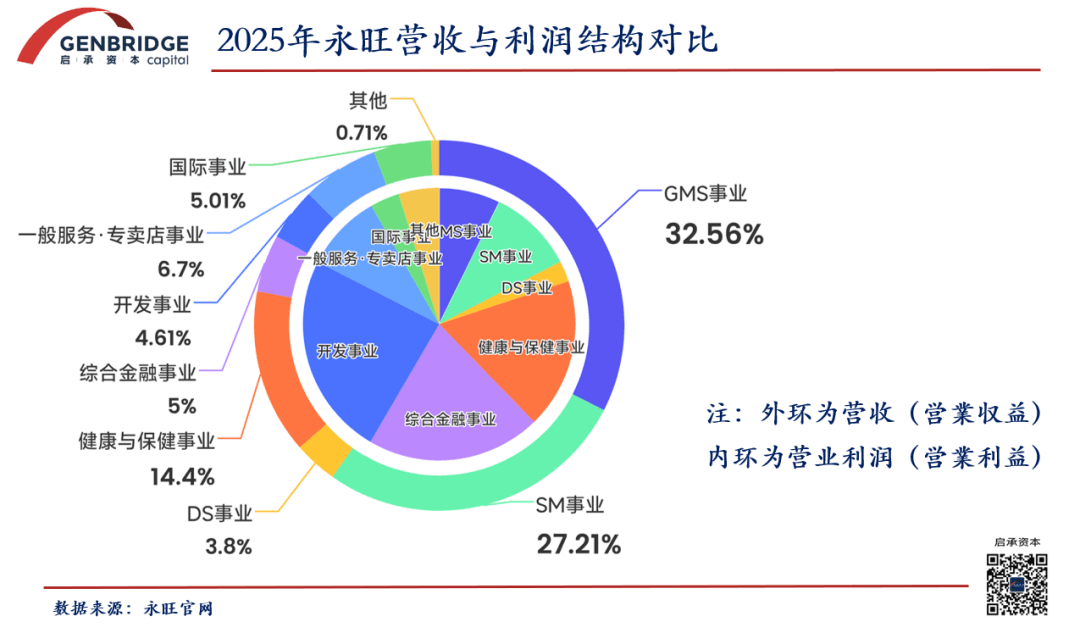

From a revenue perspective, AEON’s GMS (general merchandise store), SM (supermarket), and health and wellness businesses account for more than 60% of the group’s substantial revenue base, making it the undisputed leader in Japan’s food retail sector.

Yet from a profit perspective, the true foundation of AEON’s earnings is not traditional merchandise sales, but its financial services and commercial real estate businesses. These segments generate only around 10% of revenue, yet contribute nearly 40% of the group’s core profit.

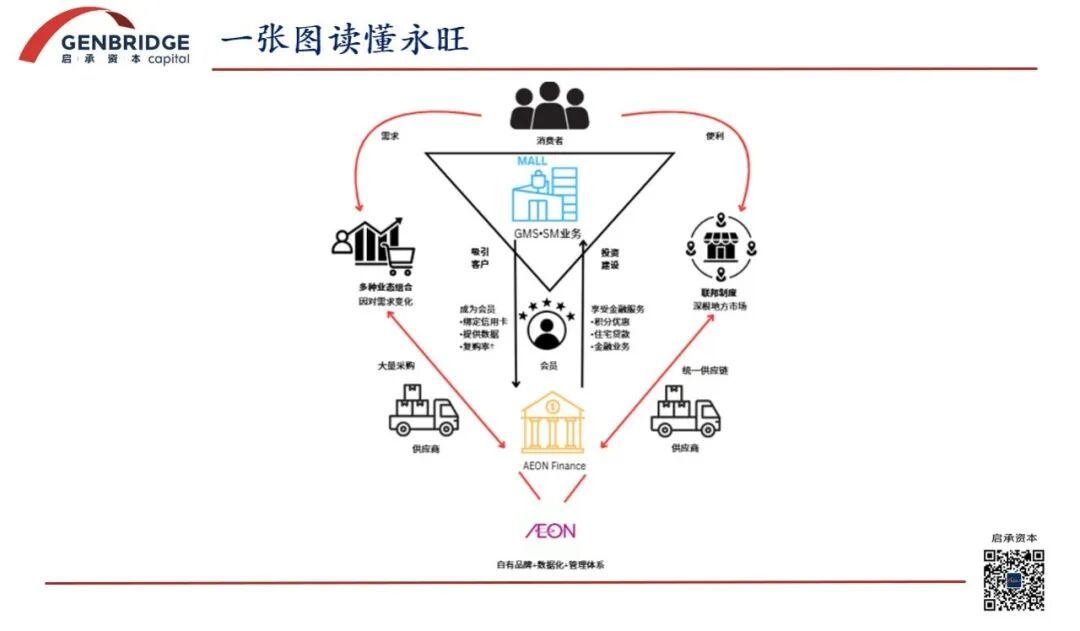

In other words, AEON is not a supermarket operator in the conventional sense. It is better understood as a platform company: retail stores serve as vast traffic gateways, while financial services, real estate operations, and frontline food supermarkets function as its core profit engines.

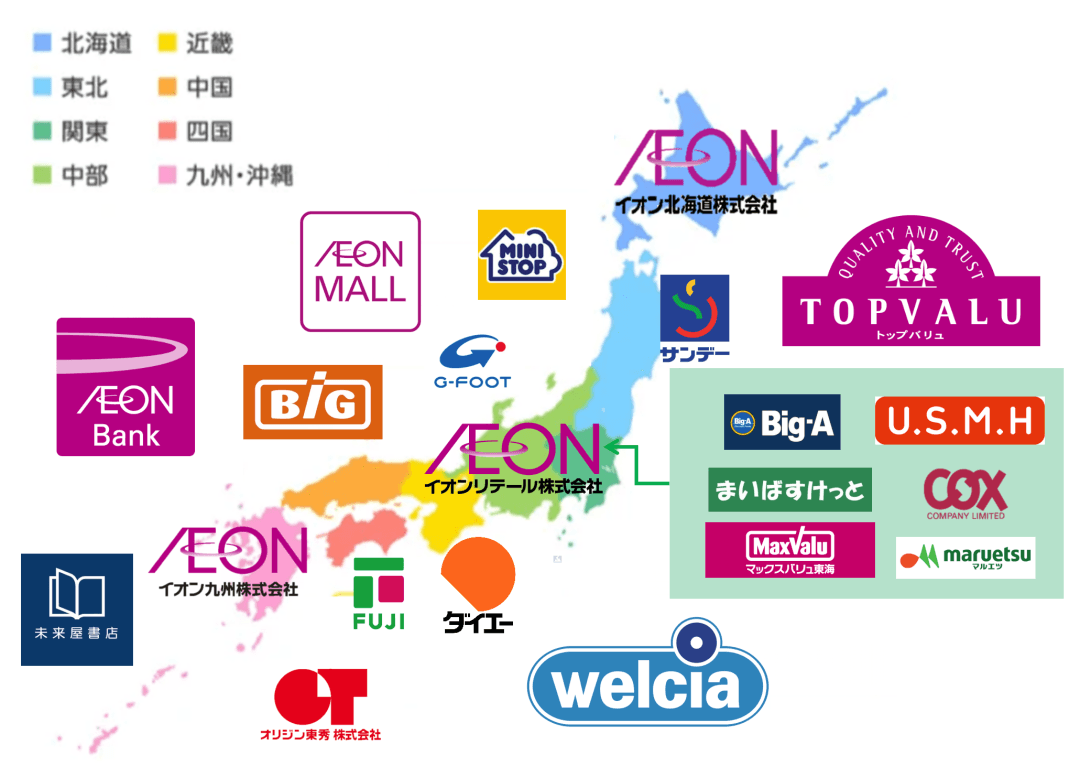

Under the AEON umbrella sit nine distinct retail formats, a vast base of 50 million stored-value members, and more than 300 subsidiaries, including nearly 20 independently listed companies....

How did AEON evolve, step by step, from a large-format retailer into a vast platform?

Simply put, AEON began as a cross-regional retail alliance. As its scale expanded, the alliance gradually integrated more resources: on the one hand, it leveraged group capabilities to connect supply chains and enhance digitalization and financialization; on the other, it continued to expand through end-of-life succession, countercyclical acquisitions, and the incubation of new retail formats, ultimately evolving into a platform-based enterprise.

After half a century of alliances and consolidation, AEON has developed into an organization that appears loosely federated. Yet it is precisely this structure—decentralized without becoming fragmented—that has enabled AEON to endure across cycles.

The advantages of AEON’s federal system

On the surface, AEON’s federal system may appear to be little more than an assemblage of regional retail leaders. In essence, however, it is an exceptionally sophisticated system of monetization and risk hedging, capable of continuous self-evolution.

Over the course of its long operation, this structure has demonstrated advantages that single-format retailers, such as pure-play convenience stores or hypermarkets, find difficult to replicate.

Advantage one: Breaking the single-format curse and building lifetime value (LTV)

In conventional retail thinking, a company can often satisfy only one dimension of consumer demand. People go to 7-Eleven for immediacy and convenience, and to Costco for weekend stock-up trips. The inherent limitation of a single-format model is that, no matter how well it performs, spending across different life stages and consumption occasions will inevitably flow to other competitors.

Through its “federal system,” however, AEON has constructed an almost airtight LTV, or lifetime value, network within regional markets.

The businesses AEON acquires or partners with across regions are not limited to general merchandise stores. They also include high-frequency, necessity-driven food supermarkets such as MaxValu and Kasumi; high-margin drugstore chains such as Welcia; and commercial real estate assets such as AEON MALL, which function as urban traffic engines.

Within the federal ecosystem built by AEON, the daily orbit of an ordinary Japanese consumer might look like this:

- After work, the consumer buys discounted bento boxes and fresh groceries at an AEON-affiliated regional supermarket, meeting high-frequency everyday needs;

- On weekends, the family goes to a suburban AEON MALL for dining, movies, and apparel shopping, covering leisure-oriented household consumption;

- When buying medicine or cosmetics, the consumer visits Welcia, the drugstore chain controlled by AEON, generating high-margin consumption;

- And connecting all of these activities is the AEON credit card in the consumer’s pocket: the AEON Card.

Through its federal system, AEON does not need to build each retail format from scratch in unfamiliar regions. Instead, it directly absorbs the leading regional players across different sectors and rapidly assembles a multi-format matrix. It draws the population of an entire region into its membership and financial ecosystem. Regardless of changes in the economic environment, consumer spending—from groceries and healthcare to leisure and financial services—ultimately circulates within AEON’s federal system.

Advantage two: Navigating the Lost 30 Years with exceptional countercyclical resilience and hedging capacity

Japan endured a prolonged and painful economic downturn. During the “Lost 30 Years,” once-prestigious department stores closed one after another, while traditional asset-heavy hypermarkets declined amid consumer downtrading. AEON, however, grew stronger through the downturn, thanks to the risk-hedging and antifragile qualities of its federal system.

The first layer is the hedging effect of its profit structure. During economic downturns, consumers do indeed tighten their wallets, placing intense pressure on the retail margins of general merchandise stores. Yet demand for essential food products rises. Within AEON’s federation, deeply rooted regional supermarkets take on the role of providing stable cash flow.

As economic conditions weaken, demand for installment payments and credit increases. AEON’s credit cards, distributed through its retail network, and its broader financial services business generate substantial interest income. Front-end retail sustains traffic, while back-end finance and real estate capture profits. This structure gives AEON remarkable resilience in difficult conditions.

The second layer is the antifragility of its organizational structure. In a highly centralized, single-entity enterprise, one flawed regional investment decision by headquarters can easily trigger a systemic crisis across the entire organization. The downfall of Daiei, for example, was closely linked to its indiscriminate expansion through land acquisitions.

AEON’s federal system, however, is decentralized. Even if a regional subsidiary incurs losses due to intensified competition or flawed decision-making, the partial independence of its finances and operations effectively contains the risk at the local level, preventing it from immediately dragging down the entire group;

At the same time, AEON headquarters, acting as the alliance leader, can rapidly mobilize shared-platform resources, such as capital injections, lower-cost private-label products, and management talent, to help the regional subsidiary rebuild.

This distributed network structure allows AEON to enjoy the scale advantages of a vast group while preserving the vitality of local enterprises, enabling it to navigate the challenges of different economic cycles with composure. During upswings, regional companies can use their autonomy to move flexibly and capture market share quickly. During downturns, they can share headquarters’ supply chain and IT costs, drawing strength from the collective.

The resilience behind AEON’s federal system

A federal system may be compelling in theory, but its true challenge lies in trust. Each regional leader is a formidable operator forged through fierce competition in the local market. Persuading them to lower their guard is far more difficult than it may appear: how should interests be distributed fairly? How can power be prevented from falling into the hands of a single party? How can different cultures coexist? Without careful management, an alliance can quickly dissolve into a fragmented coalition of competing agendas.

AEON’s internal structure of trust was not the product of a predetermined top-down design. It was painfully forged through a series of near-collapse crises.

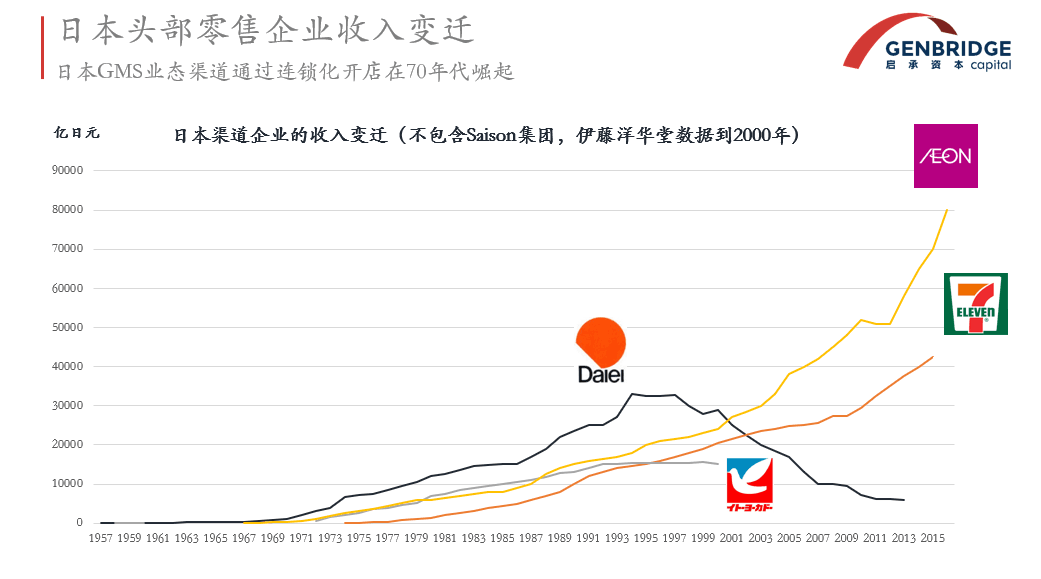

Let us turn the clock back to 1969. Japan’s retail industry was still in an untamed era in which scale reigned supreme. Daiei emerged as the dominant player, aggressively opening hypermarkets of more than 5,000 square meters across the country. By leveraging its enormous purchasing volume to drive down prices, it steadily squeezed the survival space of small and mid-sized retailers.

Faced with Daiei’s relentless advance, Okadaya, a regional supermarket based in Mie Prefecture, began searching for a path to survival. Its founder, Takuya Okada, understood that the company could not possibly endure in the shadow of a giant through its own strength alone. Rather than fight in isolation and wait to be crushed, it was better to seek strength through alliance.

Okadaya therefore joined forces with Futagi of Hyogo Prefecture and Shiro of Osaka Prefecture. The three anxious owners of small regional supermarkets sat down at the same table and agreed to form an alliance. To bring this alliance of the weak into being, Takuya Okada demonstrated remarkable breadth of vision: he relinquished both the chairman and president positions, voluntarily ceding managerial authority.

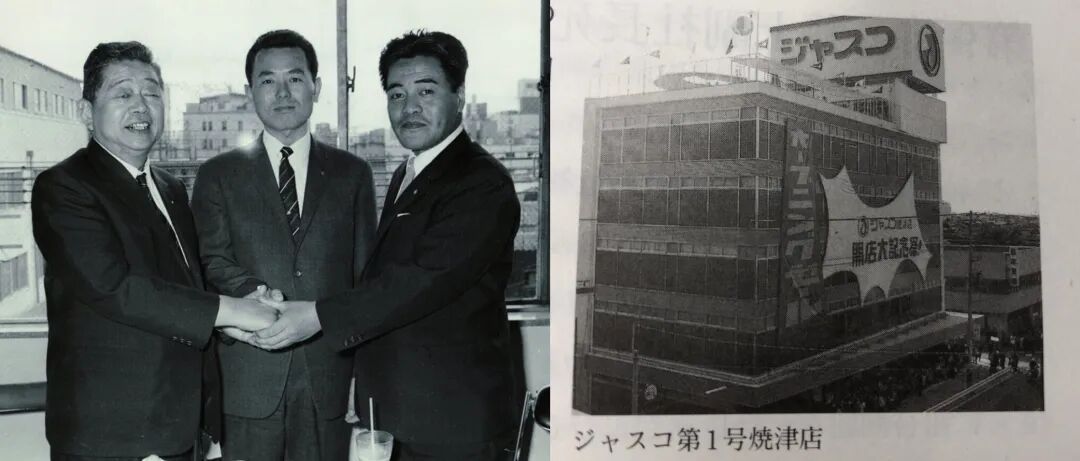

The merged entity was named Japan United Stores Company, or JUSCO. Its founders established five principles of cooperation, declaring that “future participants shall receive equal treatment” and that “all members shall ultimately merge into a single entity.” These commitments laid the foundation for the group’s subsequent expansion.

The newly merged company consolidated the functions of the original businesses. Headquarters assumed unified responsibility for building and managing shared middle- and back-office systems, including human resources, information technology, and logistics, while separating store operations from procurement. In the very year of the merger, JUSCO’s network expanded to 72 stores, propelling it into the position of Japan’s third-largest retail group. The benefits of scale were immediate.

Yet the honeymoon period of the alliance proved exceedingly brief. Only a few months later, Shiro’s founder died suddenly of a heart attack. More devastatingly, the other two partners discovered that, in order to secure an equal position during negotiations, Shiro had manipulated its performance figures, expanded its store network excessively, and concealed substantial losses and debt.

At the same time, a full-scale management crisis erupted. Employees formed an independent union with more than 500 members and brought legal action against the new company. Many former Shiro employees had relocated from other regions, lived in poor conditions, and lacked a sense of security. The fresh food division also employed a large number of long-serving staff who struggled to accept the new organizational philosophy and systems.

Looking back, Takuya Okada later described this as “JUSCO’s most painful year.” Faced with this dual crisis, Okadaya and Futagi made a counterintuitive decision: rather than expel Shiro from the alliance, they chose to shoulder its debt together, thereby preserving organizational unity.

Another pivotal figure, a woman, played a critical role in turning the tide: Chizuko Kojima, Takuya Okada’s elder sister and head of human resources.

From the earliest days of the business, Chizuko Kojima placed great importance on human-centered care. After the atomic bombing of Hiroshima, her first action was to immediately distribute severance payments and pensions to employees. On the day before Japan’s surrender, Okadaya voluntarily repurchased all outstanding shares and issued full refunds to customers holding gift certificates.

At a time when most people were focused on self-preservation, this unwavering commitment to keeping promises enabled the Okada family to accumulate its earliest reserves of trust. Later, in 1961, Kojima traveled to the United States to study Sears’ pension and employee welfare systems, seeking to understand the foundations of long-term corporate stewardship.

Faced with the trust crisis following the merger, Kojima swiftly introduced JUSCO’s pension system and founded “JUSCO University.” She made promotion pathways, examination standards, and compensation structures fully transparent for all employees, while establishing five principles: fairness, respect, change, rationality, and capability development. In time, JUSCO came to be known as “the JUSCO of education.”

The Shiro crisis left a profound lesson for future mergers: the combination of capital is only the beginning. The foundation that sustains a federation must be an organizational and human resources system built on fairness, transparency, and genuine care for people. It was precisely this infrastructure—one that respected employees and safeguarded their interests—that established AEON’s exceptional corporate credibility, giving countless regional retailers the confidence to entrust their livelihoods and legacies to the group.

The birth of “Regional AEON”

Over the following decades, as JUSCO continued to absorb regional companies such as Ogiya in Chiba Prefecture, it gradually developed an operating mechanism for its federal system. A replicable model known as “Regional AEON” began to take shape:

Following a merger, ownership of store properties was consolidated under headquarters, while regional entities could continue using them by paying rent equivalent to only 5% of book value. This separated capital-intensive real estate assets from operating businesses, freeing regional companies from onerous property-related capital expenditure and allowing them to focus their full attention on store operations;

AEON headquarters functioned as a powerful shared platform, supplying private-label products to regional companies at cost and charging only a 1.5% logistics fee. For systems support, headquarters provided advanced IT infrastructure and talent training, charging a platform service fee of approximately 3%. Yet in areas that depended heavily on local expertise, such as fresh food procurement and the selection of regional specialties, headquarters granted local businesses substantial autonomy.

Most importantly, in terms of personnel arrangements, the founders of acquired companies continued to operate their regional businesses and could even rotate into senior leadership roles at group headquarters. This strategy of preserving local authority maximized the motivation of regional enterprises. For example, after Chiba-based Ogiya joined JUSCO in 1976, its founder later became JUSCO’s chairman, while his two sons also entered the executive director ranks.

This system combined the scale advantages of centralization with the flexibility of local autonomy. As Japan’s economy entered an era of fierce competition in a mature market, its power became strikingly evident.

Entering the 21st century, JUSCO formally changed its name to “AEON.”

After the collapse of the bubble economy, companies such as Daiei fell into crisis under the weight of real estate assets and debt. AEON, by contrast, used centralized asset management and federalized operations to ring-fence property risks at the group level while preserving the operating vitality of regional companies. As a result, it developed stronger resilience and consolidation capabilities, ultimately emerging as one of the principal acquirers during the industry shakeout.

The Okada family has long passed down a guiding principle: “Do not make money from the upswing; make money from the downturn.” Since 1990, AEON has completed nearly 70 acquisitions. Most dramatically, in 2014, AEON acquired Daiei—the former industry hegemon ultimately became its subsidiary.

AEON’s acquisitions can broadly be divided into three categories:

The first is the “end-of-life entrustment” model: founders of regional family businesses, lacking successors, entrust their companies to AEON in the final stages of their lives.

The second is the “resource-dependent” model: regional leaders recognize that they cannot independently complete digital transformation and supply chain upgrades, and proactively seek AEON’s support.

The third is the “bankruptcy restructuring” model: AEON acquires bankrupt businesses at extremely low prices, then rematches retail formats based on location quality—converting prime locations into general merchandise stores and weaker locations into discount stores.

Among these three categories, two cases stand out as textbook examples of AEON’s federal system.

The Kasumi case: why would a mature supermarket operator choose to join AEON?

Kasumi is a regional supermarket operator centered in Ibaraki Prefecture. The company has a distinctive philosophy: its founder, Teruo Kanbayashi, came from a Buddhist background and sought to give back to society through retail. In the company’s accounts, revenue was referred to as the “value of repaying kindness,” while product loss was called the “value of taking life.”

In 2003, Kasumi achieved the strongest revenue and profit performance in its history. Conventional wisdom would have suggested seizing the momentum and expanding aggressively. Instead, its president made an unexpected decision that year: to sell Kasumi to AEON.

Kasumi’s president believed that Japan’s retail industry was undergoing profound change: leading domestic companies were declining, while foreign players were expanding rapidly. In the long run, regional companies would be unable to bear the high costs of IT infrastructure and supply chain upgrades, and their competitiveness in product development, store expansion, talent management, and information systems would gradually weaken. It was therefore better to seek an alliance while the business was still at its strongest: “If we wait until the downturn to seek an alliance, we will lose our bargaining power.”

Among the many potential alliance leaders, AEON ultimately won Kasumi’s trust because of its federal culture of “empowering without controlling,” its deep understanding of the supermarket business, and its strong private-label development capabilities.

In 2003, Kasumi began cooperating with AEON. Initially, AEON held only a 15% stake in the company, before gradually increasing its ownership.

In 2015, AEON formally consolidated Maruetsu, MaxValu Kanto, and Kasumi into a subsidiary, United Super Markets Holdings (USMH). The company became the largest supermarket group in the Greater Tokyo area, with 661 stores and approximately RMB 40 billion in revenue. AEON ultimately held more than 51% of its shares, while Kasumi’s president was promoted to director and executive vice president of the AEON Group.

The Welcia case: AEON’s new channel battle, from supermarkets to drugstores

After 2000, drugstore chains represented by Matsumoto Kiyoshi gradually eroded supermarket market share through dense store networks and high-frequency consumer categories. To rapidly establish its own position in the drugstore channel, AEON took an equity stake in regional drugstore operator Welcia.

To compete with the rapidly growing Matsumoto Kiyoshi, AEON took several critical steps:

First, it established a pharmacist training school at the back end, continuously supplying professionally trained pharmacists to frontline stores. This qualified the stores to sell prescription medicines;

Second, it developed the capability of “category appropriation,” or “Line Robbing,” early on, taking categories such as food, ready-to-eat products, and pet supplies from supermarkets, convenience stores, and home centers. This transformed drugstores into places where consumers could conveniently purchase a week’s worth of daily essentials. The optimal drugstore format also evolved from the early 500-square-meter model into today’s 1,000–2,000-square-meter large-format stores, equipped with 50 to 60 parking spaces.

Third, AEON provided capital support for Welcia to continuously acquire smaller regional drugstore chains, rapidly increasing store density across local markets.

In 2014, Takayuki Suzuki, one of Welcia’s founders, was diagnosed with terminal pancreatic cancer. From his hospital bed, he asked AEON president Motoya Okada to “protect the company.” In 2015, AEON increased its stake from 29.2% to 51.29%, bringing Welcia into its consolidated financial statements.

In 2014, after acquiring Shizuoka-based leaders Takada Pharmacy and CFS Corporation, Welcia secured approximately 50% of the pharmacies in Shizuoka Prefecture.

In 2025, Welcia merged with another major player, Tsuruha. Following the merger, the combined entity is expected to operate 1,850 prescription pharmacies and hold approximately 25% market share, while AEON will own a 50.9% stake in the new entity. AEON even plans to use the health-profile data accumulated from Welcia’s 43 million users to develop an AI-powered health advisory system.

At this point, AEON completed its evolution from a drugstore retailer into a “healthy living platform.” This was a full-scale replay, within a new retail format, of its federal logic: retail as the gateway, with services and data providing strategic depth.

Author’s note: Adaptation and consensus

Within AEON, there is a well-known family maxim: “Put wheels beneath the roof beams.”

The phrase may sound counterintuitive, yet it precisely captures AEON’s strategic agility. It is this deeply dialectical management philosophy that has enabled such a vast and loosely federated empire to operate efficiently for half a century.

AEON’s renowned “Scrap and Build” principle evolved from this philosophy. More specifically, AEON believes that the essence of retail lies in evolving alongside consumers. Even when a store remains profitable, if its commercial district is aging or its format no longer aligns with current demand, AEON will not hesitate to close it, demolish it, or undertake a fundamental restructuring of its format.

The ability to liquidate and relocate at any time is made possible by the asset-light operating model discussed earlier. Free from the constraints of entrenched sunk costs, each of AEON’s business units can pivot with agility through the tracks of changing times, as though mounted on wheels.

Yet underlying this extraordinary fluidity is an exceptionally steadfast ideological core.

Deeply influenced by Japan’s Sekimon Shingaku philosophy and Chōji Kuramoto, known as the “father of Japanese commerce,” AEON has consistently upheld the belief that “a store is a public institution of society.” From this perspective, merchandise inventory is merely “something temporarily entrusted to the store by customers.” By transcending the narrow notion that a company is the private property of its founder, AEON has been able to cultivate genuine public-mindedness and build an altruistic, symbiotic commercial federation through half a century of acquisitions and alliances.

In recent years, China’s retail industry has undergone a turbulent transition from an incremental market to a mature one, and from scale expansion to profitability. The path toward building nationwide offline supermarket chains remains uncertain, while omnichannel retail initiatives launched by online platforms have also struggled to gain traction.

We hope AEON’s story offers China’s retail industry a case study from a different perspective.