The most resilient commercial forces are often rooted in the everyday lives of ordinary households. A bowl of soft, fragrant rice, a steaming hotpot meal, a drop of essence oil soothing the skin, a bite of snacks bringing simple joy. These small yet real moments of happiness form the vitality of China’s consumer market.

In the recently concluded year of 2025, our listed portfolio companies delivered steady growth in their annual reports. We believe that regardless of how the environment evolves, as long as companies genuinely serve the real needs of the broadest base of Chinese consumers and remain deeply grounded, they will bear meaningful results.

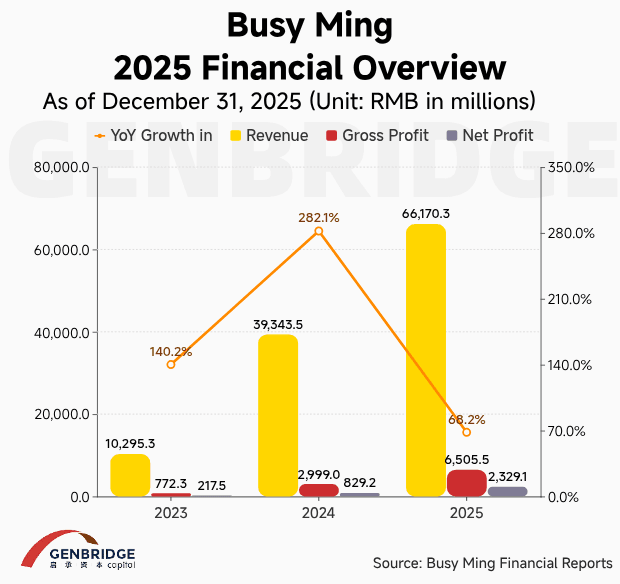

In 2025, Busy Ming Gourp, including Snack Is Busy and Zhao Yiming Snacks, reported strong results in its first annual report after listing. Store GMV reached RMB 93.57 billion, up 68.5% yoy. Revenue reached RMB 66.17 billion, up 68.2% yoy. Net profit reached RMB 2.33 billion, up 180.9% yoy, while adjusted net profit reached RMB 2.69 billion, up 194.9% yoy. Adjusted net margin improved to 4.1%, with significant gains in profitability efficiency. Key highlights over the past year are as follows:

- Store network expanded rapidly. As of the end of 2025, the total number of stores reached 21,948, with a net addition of 7,554 stores during the year, covering 30 provinces nationwide. Approximately 60% of stores are located in counties and townships, covering 1,401 counties, with a county-level penetration rate of 75%, further strengthening barriers in lower-tier markets.

- Profitability continued to improve. Gross margin from merchandise sales increased from 7.3% to 9.8%. Scale effects in procurement and logistics continued to materialize, significantly enhancing cost control capabilities. The company directly connects with more than 2,500 manufacturers and relies on 56 warehousing and distribution centers to achieve delivery to stores within 24 hours, greatly improving supply chain efficiency.

- Product portfolio continued to expand and optimize. Each store carries no fewer than 1,800 SKUs, approximately twice the average SKU count of comparable supermarkets in snacks and beverages. Among them, 34% are manufacturer-customized products. Hundreds of new products are introduced monthly, while customized small packaging and bulk options lower trial barriers and meet diverse consumer needs.

Looking ahead, Busy Ming will firmly adhere to its core strategy that good stores enable more stores, prioritizing store quality over sheer expansion. Store expansion will be based on single-store profitability and healthy operations without squeezing franchisee margins. The Chinese value snack retail market can support over 100,000 stores, and the company aims to reach 40,000 to 50,000 stores in the medium to long term, further penetrating county and township markets to enhance coverage.

At the same time, it will continue to deepen supply chain digitalization to improve warehousing and distribution efficiency and gross margins. On the product side, the company will maintain a high value for money strategy, enrich its SKU structure, strengthen its customized product capabilities, and improve store productivity and customer repurchase rates.

In the long run, the company will focus on high-quality expansion and leverage its dual-brand and omni-channel strategy to consolidate its leadership in value snack retail while achieving both scale and efficiency growth.

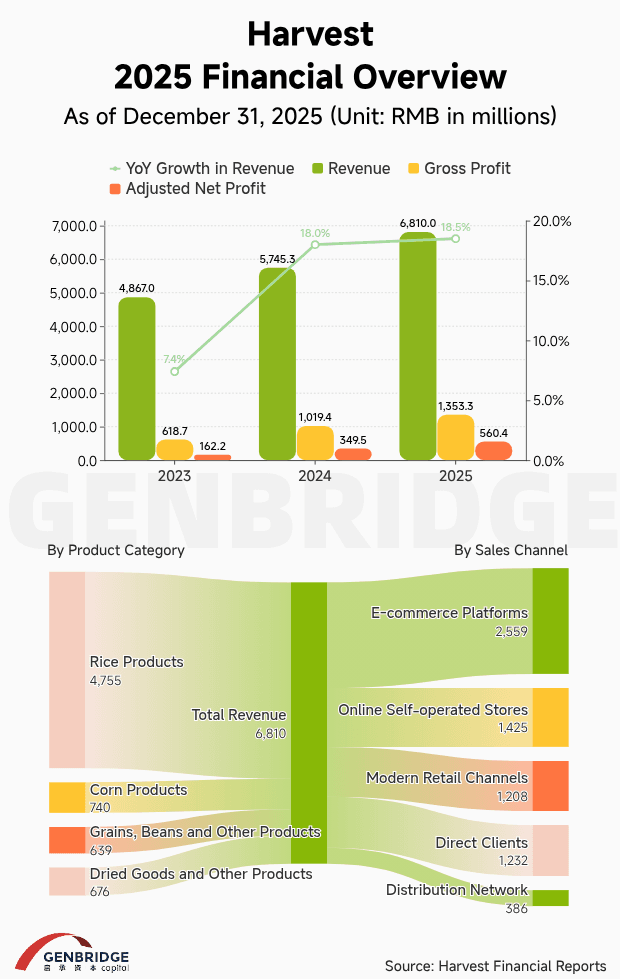

In 2025, Harvest(Shiyue Daotian Group) continued its steady growth trajectory, achieving revenue of RMB 6.81 billion, up 18.5% yoy. Gross profit reached RMB 1.35 billion, up 32.8%, with gross margin improving to 19.9%. Profit for the year reached RMB 428 million, surging 109.5% yoy, while adjusted net profit reached RMB 560 million, up 60.3%. Key financial indicators significantly outperformed the industry, with profit growth far exceeding revenue growth, demonstrating strong earnings quality. Key highlights over the past year are as follows:

- The rice products remained solid. As the core pillar, rice generated RMB 4.755 billion in revenue, accounting for 69.8% of total revenue and growing 18.4% yoy, reinforcing the core business.

- Diversified categories experienced strong growth. Revenue from grains, beans and other products reached RMB 639 million, up 36.0% yoy. Revenue from dried goods and other products reached RMB 676 million, up 51.5% yoy, driven by new product development and improved efficiency of secondary product lines.

- Omni-channel efficiency improved. E-commerce revenue reached RMB 2.559 billion, accounting for 37.6%, while online self-operated stores contributed RMB 1.425 billion, accounting for 20.9%, with continued improvements in traffic conversion efficiency. Revenue from modern retail channels reached RMB 1.2 billion, accounting for 17.7%, with stronger offline penetration and enhanced online-offline synergy.

Looking ahead, Harvest will continue to deepen its rice plus diversified category strategy, accelerate expansion into high-margin categories such as grains and dried goods, and further optimize its product mix.

Leveraging its omni-channel advantages, the company will strengthen refined operations in e-commerce and upgrade offline channels through scenario-based experiences to enhance overall channel efficiency. It will also empower agriculture through technology and continuously improve its quality control system to reinforce its leadership in rice, aiming for steady growth in both revenue and profit and building a leading full-category household food brand.

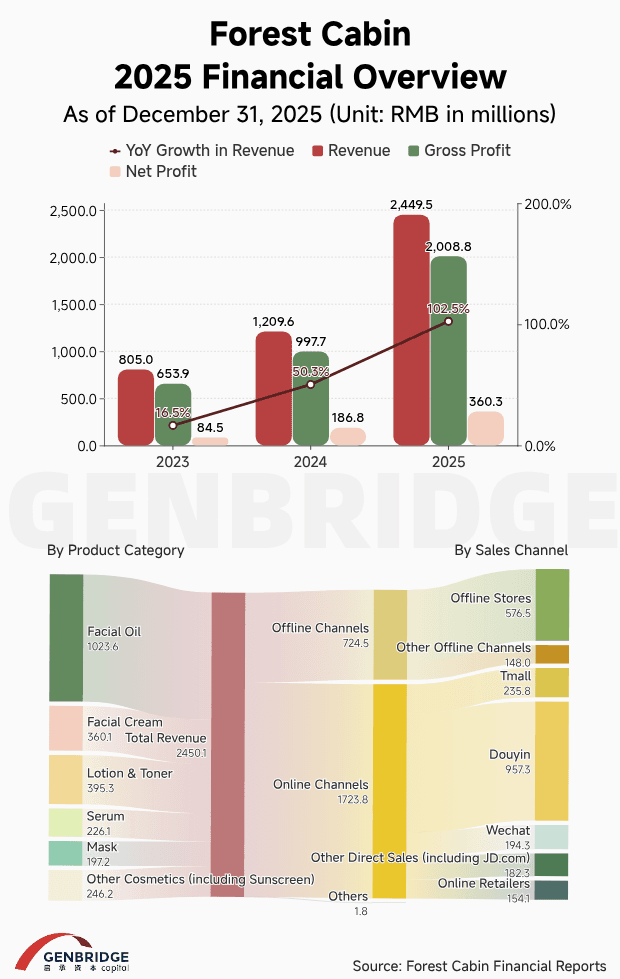

In 2025, Forest Cabin delivered strong results in its first annual report since listing, with revenue of RMB 2.45 billion, up 102.5% yoy. Gross profit reached RMB 2.01 billion, with gross margin exceeding 82%, significantly above the industry average. Profit before tax reached RMB 429 million, up 96.7% yoy, while net profit reached RMB 360 million, up 92.9%, further solidifying its leadership in premium domestic skincare. Key highlights over the past year are as follows:

- The hero product portfolio continued to scale. The camellia anti-wrinkle repair facial essence oil achieved cumulative sales of over 55 million bottles and ranked first in China’s facial essence oil category for 12 consecutive years. It generated RMB 1.024 billion in revenue, accounting for 41.8% of total sales and growing 128.68% yoy.

- A new product pipeline is taking shape. The Little Gold Pearl lotion generated RMB 204 million in revenue within six months of launch, while Black Gold Cream achieved RMB 129 million in its first year, quickly becoming core bestsellers.

- Omni-channel operations delivered strong synergy. Offline direct stores generated RMB 510 million in revenue, up 29% yoy, with average sales per store reaching RMB 1.32 million, up 13.3%. The store network reached 390 locations, with a net addition of 48 stores. Online channels leveraged platforms such as Douyin to drive traffic growth, while the OMO closed loop improved user conversion and repurchase rates.

- Scientific innovation strengthened product capabilities. Leveraging premium alpine camellia as a core ingredient and a proprietary technology system, the company launched Black Gold Cream 2.0 and new oil-based brightening product lines, enriching its portfolio and reinforcing its differentiated positioning in oil-based skincare.

The company emphasized during its earnings briefing that it will continue to follow a development path centered on scientific research and hero products, further deepening its focus on camellia as a core ingredient and building differentiated technological barriers. It will continue to expand product lines in anti-aging, repair and brightening, drive continuous iteration of hero products, and incubate more high-potential products.

On the channel side, the company will advance its omni-channel OMO strategy, using online platforms for branding and traffic while offline stores focus on experience and service, enhancing full lifecycle customer value. Management stated that it will maintain a steady and disciplined pace of store expansion, prioritizing single-store productivity and brand reputation, and building a globally competitive Chinese premium skincare brand with a long-term approach.

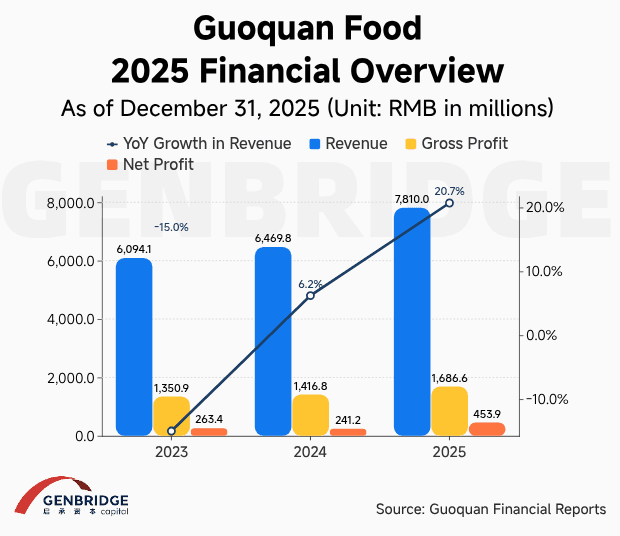

In 2025, Guoquan Food entered a phase of strong performance growth, with revenue reaching RMB 7.81 billion, up 20.7% yoy. Gross profit reached RMB 1.69 billion, up 19.0%. Net profit reached RMB 454 million, up 88.2%, while core operating profit reached RMB 461 million, up 48.2%, with core operating margin improving by 5.9%. Key highlights over the past year are as follows:

- The store network expanded with high quality. As of the end of 2025, the total number of stores reached 11,566, with a net addition of 1,416 stores. Among them, 3,010 stores are located in township markets, with a net increase of 1,004, further deepening penetration in lower-tier markets. More than 3,000 stores completed smart and unmanned upgrades, with 24-hour unmanned retail stores implemented, improving operational efficiency.

- Online channels saw strong growth. The Douyin account matrix achieved 9.41 billion impressions, while store-level GMV through Douyin reached RMB 1.49 billion, up 75.3% yoy, demonstrating strong online traffic conversion.

- Supply chain and product innovation advanced. The company launched 282 new SKUs in hotpot and barbecue categories, enriching its product portfolio. Supported by seven food production facilities and 20 digital central warehouses, it achieved rapid product circulation and continuous improvements in supply chain efficiency.

The company stated that it will continue to pursue a long-term strategy of scale with efficiency, focusing not only on store expansion speed but also on single-store profitability, store survival rates and franchisee health. It will continue to optimize store structures and promote smart and lightweight store models to improve labor and space efficiency.

At the same time, it will deepen membership operations and enhance customer spending and repurchase rates through precise marketing and scenario-based offerings. Management also noted that it will further strengthen supply chain capabilities, increase the proportion of proprietary and customized products, and improve gross margin levels.