What you are about to read is an exclusive, in-depth study of Shiseido.

In a cosmetics industry long dominated by Europe and the U.S., Shiseido, born in Asia, has stood shoulder to shoulder with global giants. It has defined beauty and style for generations and earned worldwide acclaim. Yet after its peak came a steady decline—despite multiple transformation attempts in recent years, it remains constrained and struggling.

As Chinese companies enter an era of scale, diversification, and globalization, echoes from history offer valuable lessons.

We will present the century-long corporate history of Asia’s leading cosmetics group through three in-depth articles. This is the third installment.

Author | Tojiro Kataya

Editor | Roy Zhang

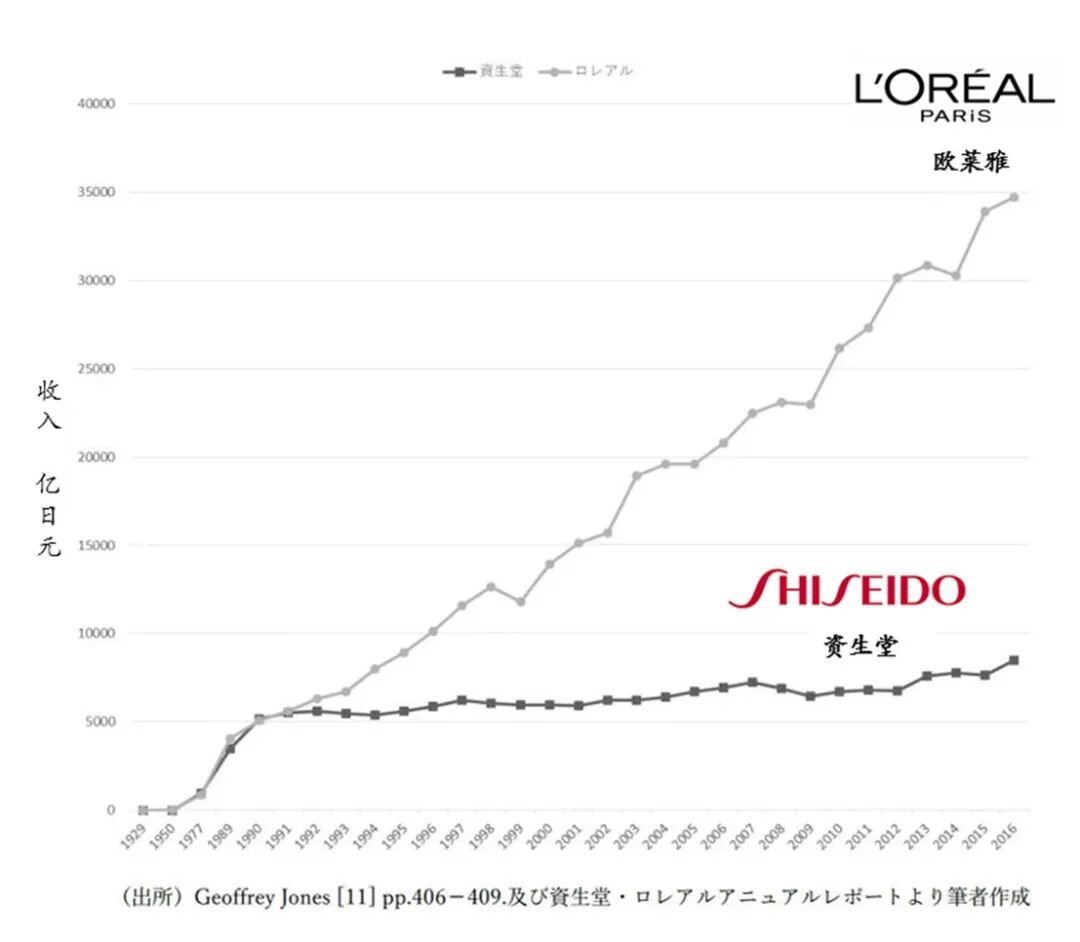

Before we begin, let us first look at a set of comparative data:

This chart offers a striking visualization of the gap: before 1990, Shiseido and L’Oréal were broadly comparable in both growth rate and revenue scale. After that point, however, Shiseido’s growth lost momentum and gradually flattened. By 2016, L’Oréal’s revenue was already more than three times that of Shiseido.

As Asia’s largest cosmetics group, Shiseido fully benefited from the tailwinds of its era and dominated Japan’s cosmetics market for more than half a century. At its peak, the number of its retail stores even exceeded that of Wallace in China today.

Yet despite such scale, after entering the 1990s, Shiseido seemed trapped under an inescapable curse, struggling in a prolonged cycle of low growth and low profitability.

In its latest 2025 financial report, Shiseido recorded net sales of approximately JPY 970 billion, down 2.1% year-on-year, marking the third consecutive year in which revenue failed to return above the one-trillion-yen threshold. Net profit attributable to owners of the parent also recorded a loss of JPY 40.7 billion, or approximately RMB 1.813 billion. Not long ago, Shiseido also lost its position as Asia’s most valuable beauty company by market capitalization to Korean company APR.

What exactly happened to Shiseido over these 30 years?

This may be one of the most compelling cases in business history. Not because Shiseido did everything wrong, but because it did almost everything right—and still failed.

When the market was advancing rapidly, it expanded with the tide. When resources were abundant, it invested early in scientific research and accumulated cultural assets. When the market turned sluggish, it cut costs and improved efficiency, launched a major-brand strategy, introduced a brand manager system, and built a DTC platform.

Each move, judged by the context of its time, was directionally correct. Every CEO saw the problem and tried to solve it. Yet the outcome was clear: none of these reforms prevented Shiseido from drifting into mediocrity.

This is the final article in GenBridge Capital’s Shiseido research series. In the previous chapters, we examined Shiseido’s journey from a street-side pharmacy to a global cosmetics empire through the lenses of brand culture and business model. In this final piece, we will reveal how the moat that Shiseido painstakingly built ultimately became the wall that trapped it.

Misfortunes never come alone

In The Sun Also Rises, published in 1926, American writer Ernest Hemingway wrote that bankruptcy happens in two ways: first gradually, then suddenly. Through the voice of a fictional character, he captured a sense of melancholy over the passing of a golden age.

By the end of the 20th century, Shiseido found itself precisely in this transition from gradual to sudden: the immense inertia accumulated during decades of golden-age growth had begun to reveal its structural flaws, while a series of external shocks abruptly pushed the company into an unprecedented existential crisis.

As noted earlier, in response to severe inventory problems, Yoshiharu Fukuhara launched the “New Shiseido” reform movement, which finally pulled the company back from its downward trajectory and restored modest growth in 1995.

However, with the collapse of the bubble economy, Japan’s consumer society officially entered a period of structural contraction. In 1994, Japan’s CPI fell below 1% for the first time, marking the end of a decades-long era of high-growth consumption.

A depiction of this period in Manga History of Japan

From 1994 to 2019, annual income among Japanese people aged 50 to 54 declined from JPY 8.6 million to JPY 6.6 million; the share of income spent on consumption fell from 80% to 60%; and the number of newborns dropped from 1.2 million to 720,000. For a cosmetics company heavily reliant on the domestic market, this meant its core customer base was shrinking systemically.

The crisis descended upon society broadly. But for Shiseido, the blow was especially severe: in 1996, the Japanese government finally abolished the “Resale Price Maintenance System” for cosmetics, known as RPM.

As discussed earlier, it was precisely the introduction of RPM that allowed Shiseido to unify retail prices through pricing agreements, protect brand margins, and fuel the prosperity of its distribution system.

At the same time, many cosmetics companies that relied on open-shelf retail and price competition gradually disappeared from the historical stage.

However, once the legal constraints were lifted, these cosmetics retailers returned in an entirely new form: the drugstores now found across streets and neighborhoods throughout Japan.

Drugstores were the product of an era of consumer democratization and price competition. Unlike Shiseido’s more than 20,000 licensed specialty stores, drugstores offered more SKUs, lower prices, and higher efficiency. Consumers no longer needed to listen to BA recommendations; they could choose products on their own. Brands could no longer directly guide offline purchasing decisions. Shiseido’s once-proud BA system became entirely ineffective in this new retail format.

This represented a fundamental transfer of channel power. In 1997, drugstores accounted for only 12% of cosmetics retail, while cosmetics specialty stores were still twice their size. Ten years later, the balance had reversed: drugstores accounted for 37%, more than three times the share of cosmetics specialty stores.

Rising alongside drugstores were affordable niche brands. In the RPM era, selling cosmetics nationwide required large-scale distribution, BA training, and heavy advertising investment—a capital-intensive game only giants could afford. But with the rise of drugstores, new brands gained an opportunity to break through the channel blockade imposed by incumbents, entering the market through price competitiveness and breakout hero products.

In particular, Japan’s OEM and ODM manufacturers also developed rapidly during this period, allowing many emerging brands to bypass lengthy R&D cycles. From concept to launch, the fastest could take as little as three months. By contrast, Shiseido, which insisted on in-house R&D and an asset-heavy model, required at least 18 months—not to mention that certain scientific outcomes could take more than a decade of investment before commercialization. What had once been “foresight” had now become a burden.

In an increasingly fast-changing market, the gap in speed became the gap between survival and decline. Shiseido had wanted to be a friend of time—but time would no longer wait for Shiseido.

How intense was market competition at the time? Major cosmetics groups launched affordable new brands one after another. Freeplus, open-shelf makeup brand KATE, functional skincare brand FANCL, and Maybelline all rose strongly during this period. Later, even Fujifilm launched the ASTALIFT skincare brand based on its imaging technologies.

Under intense market competition, Shiseido’s sales pressure rose sharply. To protect revenue, the product department blindly launched new offerings; by the mid-1990s, Shiseido was operating more than 200 brands at the same time. To meet performance targets, the sales department’s impulse to push inventory onto stores overrode everything else. The result was that, by 1997, distributor inventory turnover had once again returned to a high level of six to seven months.

This meant that Yoshiharu Fukuhara’s earlier efforts to relieve inventory pressure had largely come to nothing. The “New Shiseido” reform had failed.

The only way out

What did not kill Shiseido did not necessarily make it stronger, but it did force the system into painful self-reflection—and ultimately compelled it to pursue a genuine, fundamental transformation.

In 2005, Shinzo Maeda became Shiseido’s 13th CEO. After deep reflection, he came to a sobering realization: for more than a century since its founding, Shiseido had essentially been a B2B company. Only by transforming into a B2C brand could it survive in the new era.

How should we understand this judgment?

As discussed earlier, in the 50 years after the war, Shiseido expanded rapidly through its licensed storefront chain model and at one point controlled nearly 30% of Japan’s cosmetics market. To be fair, Shiseido had indeed pushed this commercial system to its fullest potential. Every move was designed around one objective: helping distributors sell more effectively.

BAs were, in essence, auxiliary sales personnel allocated to distributors, while the Hanatsubaki Club served as a traffic-generation tool for distributor stores. Shiseido’s true customers had never been consumers; they were distributors.

This B2B DNA produced several fatal side effects:

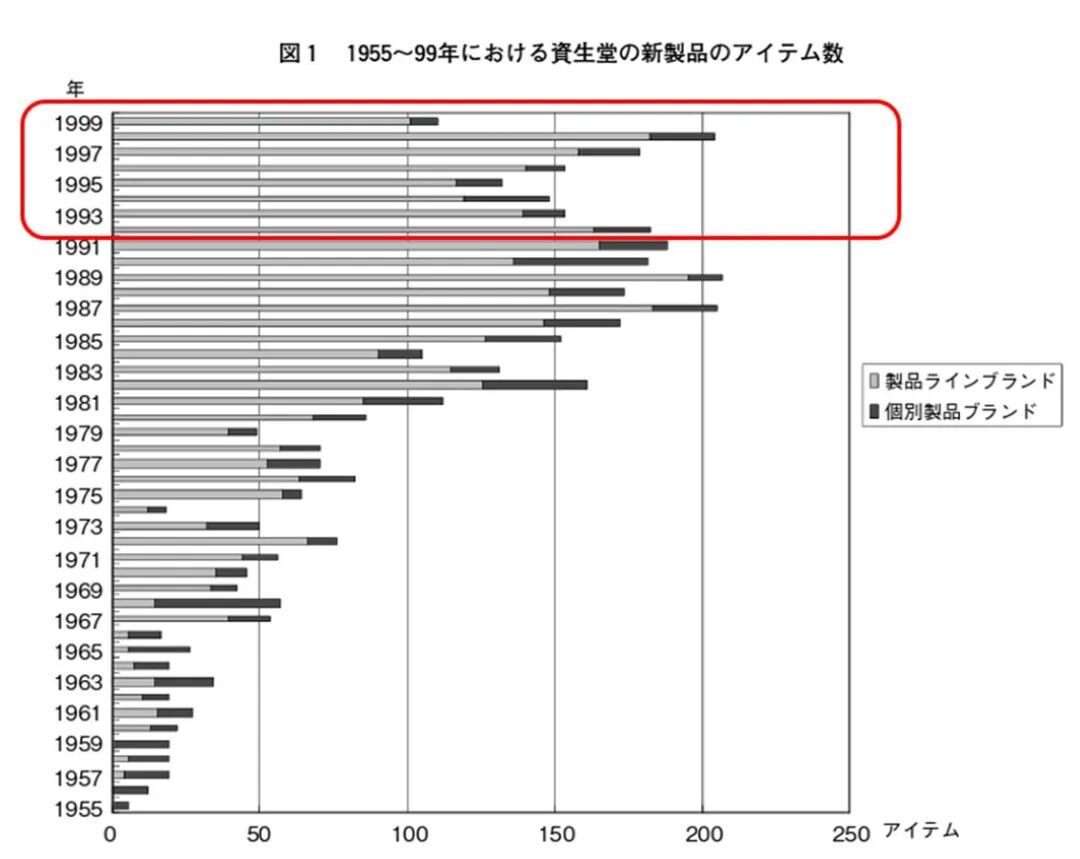

First, in order to provide distributors with marketing ammunition, Shiseido launched too many new products, severely dispersing corporate resources and making it difficult to focus on building hero products like SK-II’s Facial Treatment Essence or Estée Lauder’s Advanced Night Repair. Its persistent inventory problem was also closely related to this.

Changes in the number of new Shiseido products launched from 1955 to 1999

Second, the corporate brand and product brands became conflated. Under a B2B logic, distributors partnered with the company “Shiseido,” and consumers also purchased out of trust in the corporate name. This made sense in an era of undersupply. But in a buyer’s market, consumers care about whether “this brand is specifically designed for me” and are more willing to pay for differentiated product value. At this point, Shiseido began to lose distinctiveness. After all, when a corporate brand simultaneously represents low-end, mid-range, and high-end offerings, it effectively represents nothing clearly.

To address these problems, Shinzo Maeda launched a more radical reform, historically known as the “mega-brand” strategy.

As the name suggests, the core task of the mega-brand strategy was ruthless pruning. Shiseido originally had more than 230 brands; this time, it cut around 200 in one sweep. Among the 35 brands that made it into the final round, another six or seven would be selected as core brands for focused cultivation.

These core brands were divided into two categories:

One category followed a premium boutique route, still centered on department stores and specialty stores, such as CPB, with the goal of increasing average transaction value and customer lifetime value. To improve service quality, Shiseido even removed sales KPIs for BAs, avoiding excessive pressure on consumers and the negative sentiment it could create.

The other category followed a mass-market route, mainly targeting new channels such as drugstores, with brands such as ELIXIR and ANESSA. The goal was to occupy the shelves of emerging channels with high-momentum brands.

Shinzo Maeda’s ambition was to reshape Shiseido into an efficient modern brand management company. To that end, he initiated a deeper organizational transformation: converting the original function-based organization into a brand-centered structure led by brand managers, “making each manager fully accountable for a brand from end to end.”

Under this system, brand managers coordinated all functional departments, including R&D, design, production, and marketing, ensuring that what was ultimately delivered to consumers was a complete and coherent brand experience. This was modeled after L’Oréal’s DMI, or Direction Marketing International, system.

The climax of this reform was the launch of the haircare brand TSUBAKI.

TSUBAKI demonstrated what it meant to “make miracles through sheer force.” Shiseido cut the smaller brands in its haircare portfolio and concentrated all resources on this new brand, even deploying its precious brand symbol, the camellia. It signed six of Japan’s top young female stars at once to appear in the advertising campaign. In its first month after launch, TSUBAKI exceeded expectations with JPY 4 billion in sales and went on to hold the No.1 position in the shampoo category for three consecutive years.

At the time, everyone believed that the “mega-brand” strategy had succeeded.

A failure foretold

If you have read the previous two articles, you will know that the story was never that simple.

Sometimes, we have to admit that luck is also part of capability. Whenever Shiseido tried to regroup and regain momentum, forces beyond its control seemed to deliver a fatal blow:

In 2008, the global financial crisis broke out. In 2011, the March 11 earthquake further suppressed consumption in Japan. In 2012, the Diaoyu Islands dispute triggered a boycott of Japanese goods in China, instantly stalling Shiseido’s largest overseas growth engine. Struck by three consecutive external crises, Shiseido’s net sales plunged by JPY 30 billion in 2008, followed by years of negative growth.

But fundamentally, external crises only accelerated what was already unfolding. In the case of TSUBAKI, its failure was almost inevitable.

First, Shiseido positioned TSUBAKI as “mass premium.” Although it was sold in drugstores, it was priced 30% to 40% higher than competing products. This neither-here-nor-there positioning was deeply awkward: premium consumers would not typically buy haircare products in drugstores, while mass-market consumers became extremely price-sensitive during an economic downturn.

This misjudgment once again revealed how far Shiseido had drifted from consumers. Long-term reliance on distributor feedback for product development and iteration had deprived the company of a true understanding of consumer needs. Deeply ingrained habits of thinking could not be reversed by a single reform.

Second, Shiseido had already done everything it could to support TSUBAKI. Yet the group’s overall cost structure was too heavy, weakening its competitive efficiency in the mass market.

After seeing TSUBAKI’s success, Kao quickly followed with a competing brand, Asience, meaning “Asian beauty,” using a similar concept and a comparable level of marketing investment to challenge Shiseido head-on.

Crucially, Kao, without Shiseido’s BA system or distributor network, had a marketing expense ratio only half that of Shiseido, while its haircare revenue was ten times larger. Shiseido had little ability to fight back.

The failure of the “mega-brand” strategy was a profound regret. What made it regrettable was that the direction itself was right; yet both internal friction and external pressure pushed it away from its intended path.

Ultimately, within just three to four years of its launch, TSUBAKI fell into losses, turning from a star product into a drag on the financial statements. The brand manager responsible for it came under immense pressure and was eventually hospitalized for a mental illness. This unnamed middle manager became the person who paid the price for the failure of the entire system.

Where exactly did the problem lie?

At this point, a question naturally emerges: Shiseido was not blind to its problems, so why did its reforms fail again and again?

The answer ultimately comes down to two deep structural issues:

Problem one: the distributor system could not be changed

Shiseido’s distributor system was established in 1923. By the 2000s, it had been embedded within the company for 80 years. It had become part of the organization itself: the careers of many employees, internal processes, and mechanisms of interest distribution were all built upon this system. It was extremely difficult to sever it cleanly.

Its 25,000 distributor outlets held substantial leverage over Shiseido. These stores would instinctively resist any reform that threatened their own interests.

As early as the Yoshiharu Fukuhara era, Shiseido had attempted to implement a “format reform plan” for distributor stores, reclassifying outlets into six types based on different customer groups and usage scenarios. Yet in the end, the execution rate was only around 10%, because many long-standing franchisees simply had no desire to change. They had their own customer bases and operating rhythms—why should they go through the trouble of changing their business model? After all, even if they remained passive, Shiseido would not truly dare to cut them off.

After 2010, the rise of e-commerce brought an entirely new channel challenge. In April 2013, Shiseido launched a new online channel, Watashi Plus, in an attempt to achieve direct-to-consumer sales.

This should have been the most critical step in Shiseido’s transformation into a B2C company, but the platform encountered fierce resistance from the franchise system. Long-standing franchisees believed the online channel would damage their interests through lower pricing. In the end, Shiseido had no choice but to take Watashi Plus offline for adjustments, adding functions that redirected traffic to offline stores.

Although it was eventually relaunched, Watashi Plus had changed from a path to directly reach consumers into a traffic tool for distributors, losing the original meaning of DTC.

During the same period, Shiseido’s competitor Kosé made the exact opposite choice.

Under the strong push of its founding family, Kosé made a decisive break, cutting off all distributors and reallocating its best BA resources to the premium brand Albion. This meant voluntarily giving up a large amount of short-term revenue, but ten years later, the Kosé Group became a representative of Japan’s domestic premium beauty brands, and its overall profitability far exceeded Shiseido’s.

Over the past five years, Kosé Group’s net profit margin has ranged from 2% to 6%, while Shiseido has continued to struggle around the break-even line.

Problem two: the brand manager system never truly took root

One of the central priorities of the “mega-brand” strategy was to establish a brand manager system. This was the organizational foundation for Shiseido’s transition from B2B to B2C.

Harvard Business School professor Alfred Chandler once proposed a classic thesis: “structure follows strategy.” In other words, when a company diversifies across businesses or geographies, a divisional structure is more efficient than a traditional functional structure—each business unit holds autonomous operating decision-making power, while headquarters focuses on strategic planning and resource allocation.

The brand manager system is the concrete evolution of this logic in the consumer goods industry: each brand functions as an independent business unit, with the brand manager coordinating end-to-end decisions from product development to market launch.

At L’Oréal, for example, this system requires each brand headquarters to be located in the birthplace of the brand. Brand managers begin with consumer insight and lead the entire process from concept to launch. They do not tell R&D to “make a color-protecting shampoo”; instead, they say, “Please solve consumers’ color-protection needs in the haircare scenario,” leaving R&D to determine the product form. In key regional markets, L’Oréal also established DMI hubs to collect local consumer insights and feed them back into the global system.

However, what Shiseido ultimately created could only be described as a “localized version” that resembled the form but not the spirit. Within Shiseido’s deeply entrenched culture of functional silos, it was more like a foreign organ grafted onto the body, never truly integrated with the host.

Its greatest flaw was that brand managers were not fully responsible for the profit and loss statement and lacked key decision-making authority. Their supposed coordinating role existed in name only.

The design department pursued aesthetics, the sales department pursued distribution, and the R&D department pursued technical highlights; each department exerted influence from its own standpoint.

More absurdly, the marketing strategies for skincare products targeting young women were often determined by middle-aged male managers who did not understand this group. The products that resulted were naturally incoherent.

The deeply rooted hierarchy and bureaucratic culture were equally reflected in globalization.

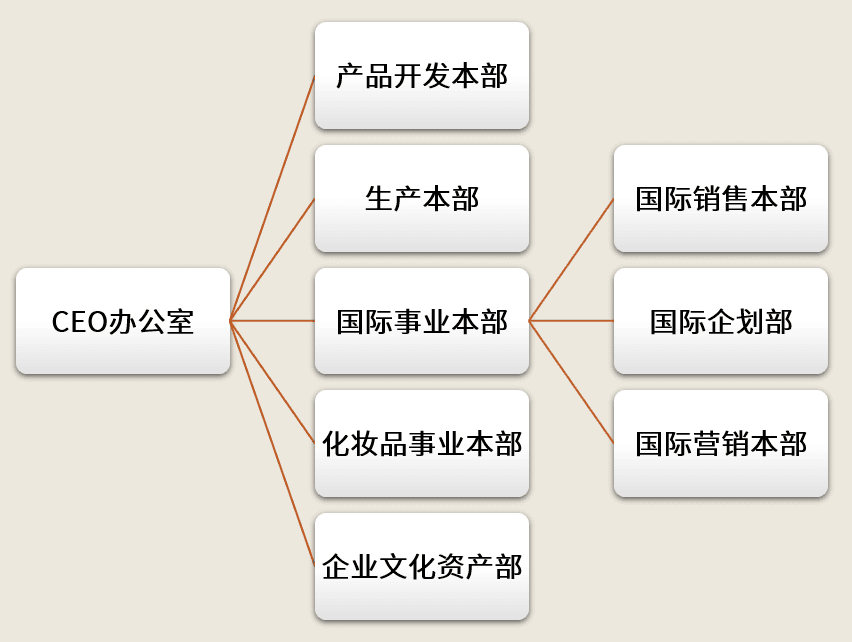

This is a simplified diagram of Shiseido’s globalization organizational structure in 2003:

As we can see, under the CEO sat functional departments such as product development, production, and the international business division; the international business division then governed operations in each country. This meant that all overseas decisions first had to be consolidated within the international business division and then approved by the CEO. Faced with complex decisions involving dozens of countries and hundreds of brands, this centralized structure was extraordinarily inefficient.

It is therefore not difficult to understand why nearly all of Shiseido’s numerous acquisitions over the past 30 years failed.

The most painful failure was the 2010 acquisition of the U.S. mineral makeup brand Bare Escentuals. Bare Escentuals’ core channel was television shopping, but Shiseido understood neither TV shopping nor how to operate omnichannel retail in the U.S. It even missed the transformation window of the mobile internet era. In the end, not only did the USD 1.8 billion spent on the acquisition come to nothing, but the company also incurred an additional USD 300 million in losses.

In 2019, Shiseido acquired Drunk Elephant for USD 845 million. Yet the brand failed to adapt to the Japanese market. Starting in 2024, its sales declined sharply; in 2025, sales were discontinued, and it became the largest drag on Shiseido’s losses that year.

Ironically, the only acquisition that survived and succeeded was the U.S. makeup brand NARS, acquired in 2000. The reason was precisely that Shiseido did not interfere with it. NARS was able to retain its full founding team, independent product cadence, and autonomous market strategy, allowing it to adjust at any time according to local market needs.

Looking at these two problems together, we can see that Shiseido was trapped:

Because it failed to establish a thorough brand manager system, the company could not build a consumer-centered decision-making system.

Because distributors constrained the company, any attempt to bypass them and reach consumers directly would be killed in the cradle.

Then was it possible for Shiseido to act more decisively and truly cut into its rigid organizational structure and distributor system?

Unfortunately, it was extremely difficult.

If your memory is good enough, you may recall that 80 years earlier, Shiseido, struggling to survive during the war, raised substantial financing from distributors in order to stay alive. This greatly diluted the founding family’s shareholding. Shiseido did not have a major shareholder capable of forcefully driving long-term transformation, nor did it fully establish a stable governance structure. Its CEOs could only make difficult trade-offs among respecting the legacy of their predecessors, responding to current performance pressures, and balancing internal factions.

This is the deepest helplessness of Shiseido.

A new round of repairs

After 2010, a consensus had already formed within Shiseido: relying on insiders alone would no longer be enough to overcome the problems inherited from history; new blood had to be brought in. Thus, in 2014, Shiseido made the boldest decision in its 152-year history—appointing its first external CEO.

The new CEO, Masahiko Uotani, an MBA graduate from Columbia University and former CEO of Coca-Cola Japan, was a renowned brand manager in Japanese business circles. He launched version 2.0 of the mega-brand strategy, pushing Shinzo Maeda’s reforms even further:

He divested the mass haircare business, which accounted for only 6% of total revenue, and concentrated resources on core brands such as CPB and IPSA; comprehensively studied L’Oréal, brought in around one hundred new executives from foreign companies, and sought to fully implement the brand manager system; and reorganized the business into six regions—Japan, China, Asia, the U.S., Europe, and travel retail—while decentralizing decision-making authority.

As a result, Shiseido reached a turning point. Revenue broke through the one-trillion-yen mark, rising from JPY 770 billion in 2014 to JPY 1.13 trillion in 2019.

然而,2020年全球疫情严重冲击了化妆品市场,资生堂再次面临乱价危机,加之没能抓住中国市场内容电商的新趋势,中国区业绩也一路下跌。2025年,资生堂的财报又出现了407亿日元的净亏损。

However, in 2020, the global pandemic severely disrupted the cosmetics market, and Shiseido once again faced a price disorder crisis. Coupled with its failure to capture the new trend of content commerce in the Chinese market, performance in China also declined continuously. In 2025, Shiseido’s financial report once again recorded a net loss of JPY 40.7 billion.

In early 2025, the new CEO, Kentaro Fujiwara, took office. According to our understanding, he is adjusting the influence of foreign-brand-style managers, seeking to use Shiseido’s own cultural assets as the driving force, and attempting to develop a methodology known as “The Shiseido Way.” For a century-old company with deep accumulated heritage, this may be a constructive direction.

Author’s note

Before beginning this research, I had assumed that a company with Shiseido’s long history would, like Toyota and other major enterprises, have its own distinct processes and methodology. Yet to my surprise, after speaking with multiple former Shiseido employees, no one could clearly articulate what exactly constituted “The Shiseido Way.”

Influenced by Japan’s lifetime employment system, people rarely questioned established workflows, and much of the work relied on tacit understanding. Whether in product development processes or organizational culture frameworks, there seemed to be no clear internal consensus. Against this backdrop, the arrival of foreign-company-trained managers was bound to trigger strong organizational rejection.

Therefore, I strongly agree with the new CEO’s attempt to search for “The Shiseido Way.” After all, during Japan’s “Lost 30 Years,” Shiseido still managed to maintain slow growth and avoid being eliminated, which in itself proves the compounding effect of its cultural assets.

A friend once shared an experience with me: while vacationing in a remote village in Japan, she met an elderly, white-haired BA at a local Shiseido specialty store. Even though she was already over 70, the BA still enthusiastically explained scientific skincare techniques to Chinese tourists, continuing to contribute value to the work she had loved for a lifetime.

I think perhaps this is what is most precious about Shiseido: its reverence for beauty, vitality, and the bonds between people.

The essence of cosmetics is “emulsification”—the stable blending of water and oil. I hope that one day, Shiseido will also be able to steadily blend its accumulated historical and cultural heritage with the brand management capabilities required by the new era. As the American writer F. Scott Fitzgerald once said:

“The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.”

References

Yasuto Ida. A Business-Historical Study of Major Cosmetics Manufacturers. Koyo Shobo, 2012.

Yuji Akamatsu. Brand Strategy in the Cosmetics Industry: A Comparative Study of Cosmetics Companies in Japan and Korea. Osaka Metropolitan University Press, 2018, revised edition 2020.

Yoko Kawashima. The Shiseido Brand: The Ever-Evolving Secret of “Beauty”. Bungeishunju, Bunshun Bunko, 2010.

Manabu Yamamoto. The Evolution of Shiseido: The China Market and Mega-Brand Strategy. 2010.

Yoshito Kakimoto. “Shiseido’s Market Segmentation Strategy from 1982 to 1999: From the Perspective of Pricing.” 2012.

Ning Liu and Takaho Ueda. “Shiseido’s Successful Global Expansion in China.” Marketing Journal, 2004.

Sho Harada. “Shiseido’s Global Brand Management.” Distribution, 2008.

Shuichi Kishimoto. “Shiseido’s Marketing and Distribution.” Kanazawa Seiryo University, 2014.